NGS offering

NGS Super members can invest in:

- MySuper: In the Diversified (MySuper) investment option within the NGS Super Accumulation product

- Choice: within the:

- NGS Super Accumulation product (11 investment options)

- NGS Super Transition to Retirement product (11 investment options)

- NGS Super Income Account product (12 investment options).

Determination for the period ending 30 June 2025

Our performance assessment for the year ending 30 June 2025 is outlined below.

MySuper determination

The Trustee has determined that NGS Super is promoting the financial interests of the Fund’s beneficiaries in relation to the outcomes of the MySuper product. Furthermore, it determined that:

- Members are not being disadvantaged by the scale of the Trustees business operations.

- The operating costs are not inappropriately affecting the financial interests of members.

- The basis for the setting of fees is appropriate for members.

- The options, benefits and facilities offered are appropriate for members.

- The investment strategy, including the level of investment risk and return target, is appropriate for members.

- The insurance strategy is appropriate for members.

- The insurance fees charged do not inappropriately erode the retirement incomes of members.

Choice determination

The Trustee has determined that NGS Super is promoting the financial interests of the Fund’s beneficiaries in relation to the outcomes of the choice product. Furthermore, it determined that:

- Members are not being disadvantaged by the scale of the Trustees business operations.

- The operating costs are not inappropriately affecting the financial interests of members.

- The basis for the setting of fees is appropriate for members.

- The options, benefits and facilities offered are appropriate for members.

- The investment strategy, including the level of investment risk and return target, is appropriate for members.

- The insurance strategy is appropriate for members (Accumulation Account only).

- The insurance fees charged do not inappropriately erode the retirement incomes of members (Accumulation Account only).

Annual determination: 30 June 2025

Our strategic objectives have been designed to promote positive member outcomes and support the sound and prudent management of our business operations. The Fund follows sound risk and governance practices, aiming to ensure that member outcomes are not jeopardised by incidents of loss, reputational damage, or inappropriate decision-making. The assessment of our performance is based on these guiding principles.

Measure and compare products

The metrics for our assessment of the Diversified (MySuper) investment option are prescribed by the Australian Prudential Regulation Authority (APRA). We have assessed our performance against our strategic objectives and member outcomes targets and compared ourselves against other Australian Funds using APRA data.

For Choice, we have used the data from SuperRatings as the basis for our assessment. Investment options were mapped to the most relevant SuperRatings Index, and we compared our returns over 1, 3, 5 and 10-year periods against all options in the relevant index.

Investment performance

Our objective is to provide investment options to meet a range of member needs, while ensuring that no option has excessive costs or performs inadequately over the longer term.

Level of investment risk

We design our investment menu so that members have diversification across asset classes and risk/return profiles. Our options are designed to perform well in the medium to long term, with lower volatility of outcomes in the short term.

Fees and costs

Our objectives are to provide products and services at a fair cost, and at a fee structure that is sustainable to ensure we can continue to deliver appropriate member services.

Product appropriateness for our membership

We have assessed our performance against our strategic objectives and member outcomes targets and compared ourselves to peer groups using APRA and SuperRatings data. The following assessment factors have been used:

Options, benefits and facilities

Our objective is to ensure that products and services offered are tailored to the Fund’s specific membership. Therefore, NGS Super aims to offer products that provide options, benefits and facilities reflecting the needs of this specific membership, which are integrated and simple to understand and navigate.

We design our products and services to enable our members to get the most from what we offer by ensuring easy access to the information and help they need, at the right time, via their most convenient channel (digital, phone-based and face-to-face). Furthermore, we believe sound financial advice empowers members to make decisions and take actions that lead to better retirement outcomes.

The options, benefits and facilities offered by the Fund are the same for both our MySuper and Choice products.

As part of the broader member product offering, the Board concludes that the options, benefits and facilities offered by the Fund support the determination that the Fund promotes the financial interests of the beneficiaries.

Investment strategy

The Fund’s suite of investment options have had strategies designed to provide members with choice based on their individual risk appetite and investment time horizon. In addition to the pre-mixed options, members have the building blocks to construct a tailored investment strategy based on personal preferences. This includes access to a number of sector specific options as well as access to a direct investment platform (providing a range of ETFs, Term deposits and direct equity investments)*. Construction of a member’s tailored option may be undertaken by the member or with the assistance of an NGS Super or external financial planner.

*This feature was removed on the 30th of May 2025.

The Diversified MySuper option has been designed for the diverse range of NGS members giving consideration to the fund memberships’ age, gender, account balance and expected retirement age distributions. The resulting MySuper investment strategy is expected to achieve growth over the medium to long term that exceeds inflation by more than 3%. Furthermore, the option is diversified across countries, industries, sectors, currencies, and underlying companies and assets to ensure the prospects of achieving returns are not hindered by concentration risk in any one area. This composition reduces the impact of market shocks. The asset allocation is adjusted to accommodate the economic conditions and regularly reviewed to ensure it remains appropriate.

As a default option – the Diversified MySuper option remains appropriate as it provides a good amount of capital preservation qualities whilst also providing exposure to growth over the medium to long term. With fund members more likely to remain within the workforce longer than the average worker and longevity risk increasing, the portfolio must maintain “all weather” properties to help members grow their retirement savings over time, whilst reducing the sequencing risk associated with large market drawdowns.

The full suite of investment options provides members with a range of pre-mixed options to meet different risk preferences, whilst also providing asset class building blocks for members wishing to tailor their options further. The blend of this suite of options and the strategies developed for each option ensure the choice products remains appropriate for our members.

Insurance strategy and premiums

Our objectives are to provide group death, total and permanent disability (TPD) and income protection cover which is appropriate to the needs of our membership, and to offer sustainable premium rates. We strive to be at the forefront of fair, helpful and timely service.

The Fund’s insurance strategy is based on providing an insurance design that:

- reflects the insurance needs and demographics of different groups of members

- aligns to the needs of the target membership, while offering the flexibility for members to tailor cover to their specific needs

- offers Death (including terminal illness), Total and Permanent Disability (TPD) and Income Protection (IP) benefits as a default, and

- balances the cost of premiums with the levels of cover provided, while limiting cross-subsidies between members.

The Fund’s insurance arrangements are the same for both MySuper and Choice accumulation members.

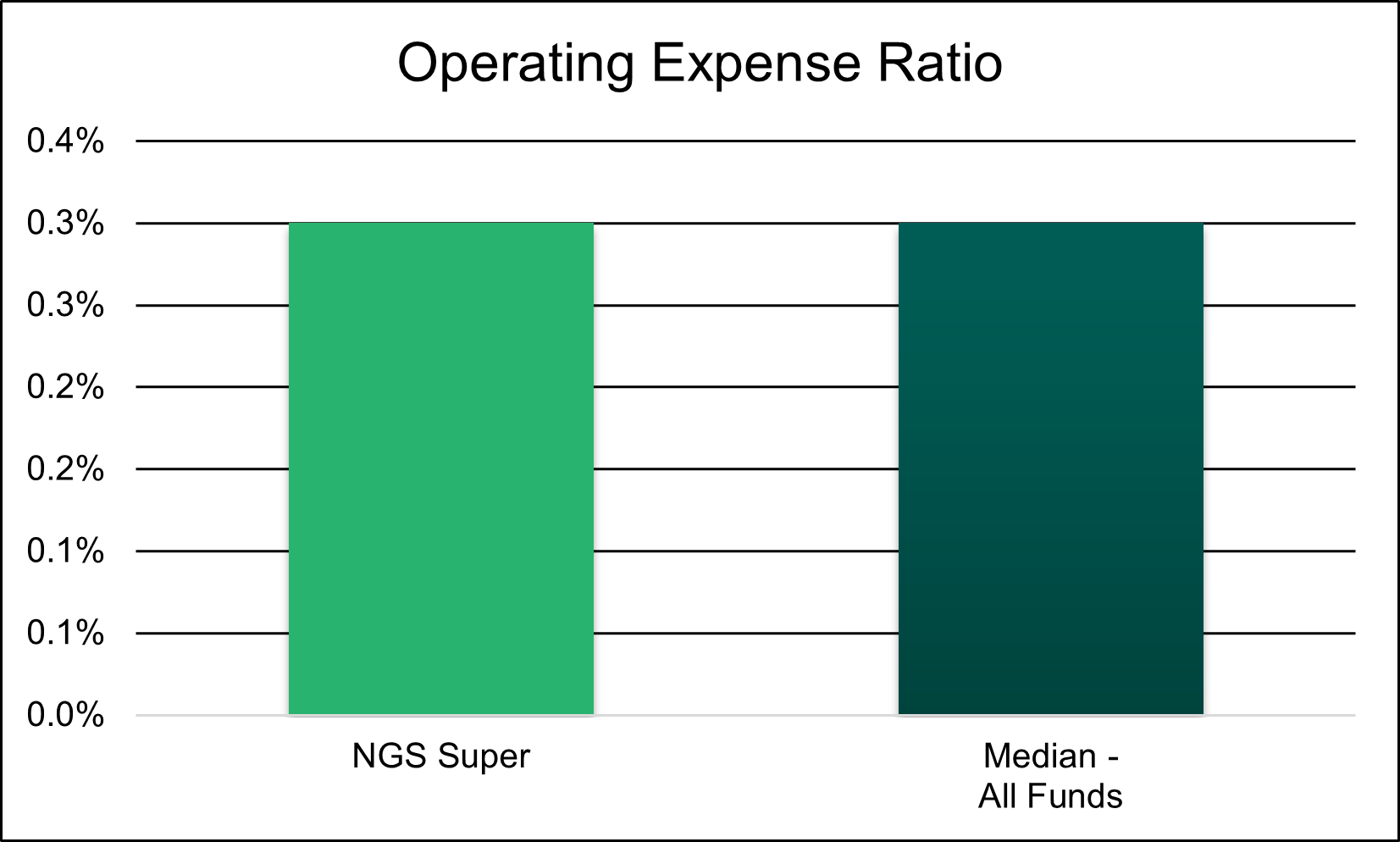

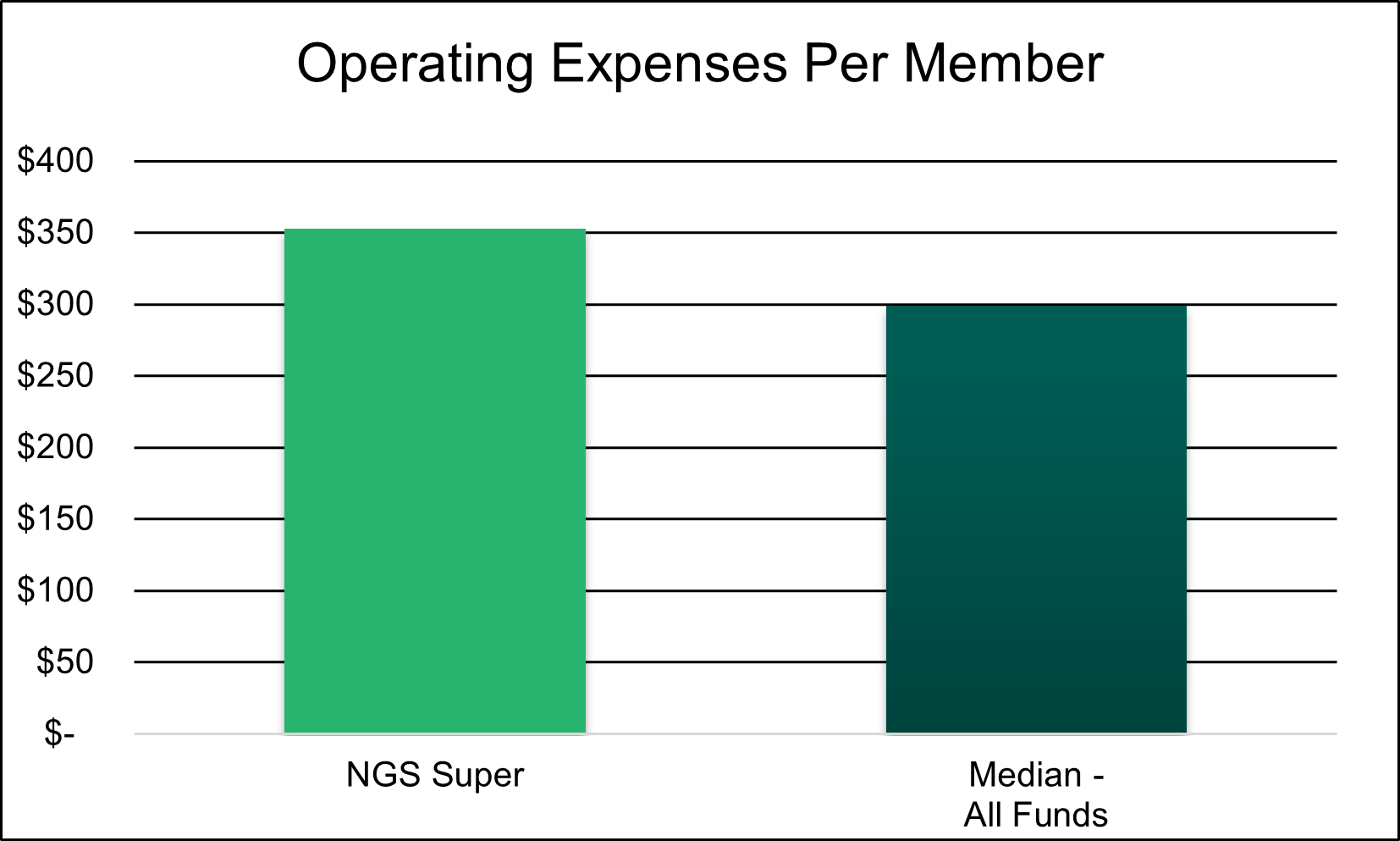

Scale and operating costs

Our objectives are to seek opportunities to obtain scale advantages through both organic and inorganic growth. We also aim to conduct our operations efficiently, and in a manner which maintains operating costs at a reasonable level for the services provided to members.

The Fund pursues scale only when it adds clear value to members, such as cost savings, better investment opportunities, and enhanced services. NGS Super is committed to operating efficiently, keeping costs reasonable relative to the services provided. Annual budgets are carefully planned and monitored by the Board, with project costs reviewed thoroughly before approval. Outsourced providers are used as needed to maximise expertise and efficiency.

Below are key metrics demonstrating NGS Super’s cost-effectiveness, including the Operating Expense Ratio and Operating Expenses per Member.

Fee strategy

NGS Super aims to provide products and services at a fair cost. We promote internal efficiencies to contain operating costs, whilst accepting higher investment costs through active investment strategies which are directed toward achieving higher net returns. NGS Super offers a competitive fee structure, which is derived through balancing various competing factors. While the NGS dollar-based administration fee remained slightly above the competitor median, the percentage-based admin fee remained below median, even as competitor funds applied changes to reduce dollar-based fees in favor of percentage-based fees. Our assessment concludes that our fee strategy promotes the best financial interests of our members.